Working capital loans are short-term business finance products designed to cover day-to-day operational expenses when cash flow is delayed or uneven. With £23.4 billion in late payments hitting UK SMEs in 2023 alone, the demand for this type of funding has never been higher. FCA-regulated brokers like V4B Business Finance, platforms like Swoop, and specialist lenders like Rangewell all offer access to working capital loans UK businesses can draw on quickly. Typical loan amounts run from £5,000 to £500,000, with decisions often available within 24 to 48 hours for unsecured products.

What are working capital loans and how do they work in the UK?

Working capital loans are short-term finance products that cover operational costs rather than long-term investments. Think payroll, stock purchases, utility bills, VAT payments, or bridging the gap between sending an invoice and receiving payment. They are not designed for buying property or major equipment. That distinction matters because lenders assess them differently from capital expenditure loans.

The term “working capital finance” is the recognised industry phrase, though many business owners search for it simply as a business loan for cash flow. Both terms describe the same core product. Loan terms typically run from three months to five years, with APRs between 6% and 25% depending on your credit profile and trading history. The speed of access is one of the biggest draws. Some unsecured products deliver funds within 24 hours of approval.

What types of working capital loans are available in the UK?

The UK market offers several distinct products under the working capital umbrella. Each suits a different cash flow situation, so understanding the differences saves you money.

- Unsecured term loans: A lump sum repaid over a fixed period. No collateral required, though lenders may still ask for a personal guarantee. Good for predictable, one-off cash needs.

- Revolving credit facilities: A pre-approved credit line you draw from and repay as needed. Interest applies only to what you use. Ideal for businesses with recurring but unpredictable cash gaps.

- Merchant cash advances: Repayments are taken as a percentage of your card sales. Suited to retail and hospitality businesses with strong card turnover. You can read more about how this compares to other products in this merchant cash advance comparison.

- Invoice financing: Releases up to 90% of unpaid invoice value within 24 hours. Particularly useful for B2B businesses waiting on slow-paying clients.

- Business credit cards: Lower credit limits but useful for small, recurring expenses. Often come with rewards or interest-free periods if managed carefully.

All of these products are used only for operating expenses, not long-term capital investment. Using short-term finance to fund long-term assets is one of the most common and costly mistakes SME owners make.

Pro Tip: Rather than taking one large loan, consider layering finance types to match each cash flow need. For example, use invoice finance for your main receivables gap and a small unsecured loan for urgent operational costs. This approach often reduces your total borrowing cost.

Who qualifies for working capital loans and what do lenders require?

Lenders assess working capital applications differently from standard business loans, and knowing what they look for puts you in a stronger position.

- Trading history: Most high street banks and mainstream lenders want to see 12 to 24 months of trading. Alternative lenders are often more flexible, but they charge more for that flexibility.

- Annual turnover: A minimum of £100,000 annual turnover is a common threshold. Some specialist lenders accept lower figures for newer businesses.

- Credit score: Both your business credit score and your personal credit history are reviewed. A poor personal credit score can affect approval even for business loans.

- Cash flow management: Lenders want to see that you understand your cash position. Erratic or unexplained cash movements raise concerns.

- Purpose of borrowing: Be specific. Lenders view cash flow gaps as management signals. A clear explanation of why the gap exists, whether seasonal demand, delayed client payments, or a large upcoming tax bill, builds confidence rather than doubt.

Newer businesses or those with lower turnover are not automatically excluded. Platforms like Swoop and Rangewell work with a panel of lenders, including those who specialise in early-stage or lower-revenue businesses. The trade-off is usually a higher interest rate or shorter repayment term.

Pro Tip: Prepare a simple cash flow forecast before you apply, even if it is just a spreadsheet covering the next three to six months. A clear cash flow forecast demonstrates to lenders that you understand your business finances and have a credible repayment plan. This single step can meaningfully improve your approval chances.

How to compare and choose the best working capital loan for your business

Choosing between business loan options in the UK comes down to four factors: cost, speed, flexibility, and risk. Getting the balance right for your specific situation matters more than chasing the lowest headline rate.

High street banks offer lower interest but require longer trading records and take more time to process applications. Alternative lenders move faster and accept a wider range of businesses, but their overall cost is typically higher. Neither is universally better. The right choice depends on how urgently you need funds and how strong your financial profile is.

The full cost of a working capital loan includes more than the interest rate. Watch for origination fees, early repayment charges, and debentures. Some loans marketed as “unsecured” still carry personal guarantees, which means your personal assets could be at risk if the business defaults. Always read the legal agreement in full before signing.

| Loan type | Typical cost | Speed of access | Collateral required | Best suited to |

|---|---|---|---|---|

| Unsecured term loan | 6%–25% APR | 24–72 hours | Personal guarantee possible | Predictable one-off expenses |

| Revolving credit facility | Variable, interest on drawdown | 1–5 days | Rarely required | Recurring cash flow gaps |

| Merchant cash advance | Factor rate, not APR | 24–48 hours | None (card sales used) | Retail and hospitality businesses |

| Invoice financing | 1%–3% of invoice value | Within 24 hours | Invoices as security | B2B businesses with slow payers |

| Business credit card | 20%–30% APR typical | Immediate | None | Small recurring operational costs |

Pro Tip: When comparing loans, always ask for the total repayable amount, not just the monthly payment or headline rate. Two loans with the same monthly cost can have very different total costs depending on term length and fee structures.

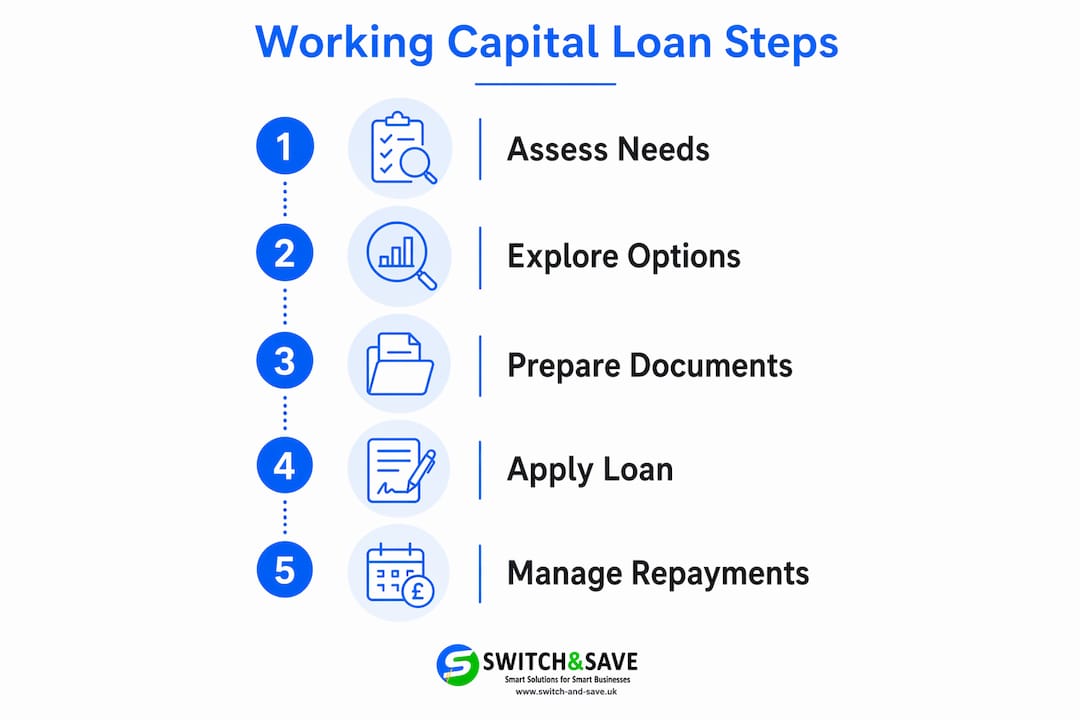

How to apply for working capital finance and manage repayments

A well-prepared application moves faster and attracts better terms. Here is what most lenders will ask for, and how to handle the process once you have funding in place.

Documents you will typically need:

- Last 6 to 12 months of business bank statements

- Most recent set of filed accounts or management accounts

- Proof of turnover, such as VAT returns or sales reports

- A cash flow forecast covering the loan repayment period

- Details of any existing business borrowing or credit facilities

- Director identification and proof of business address

The application process with alternative lenders and broker platforms like Swoop or Rangewell is often fully digital. Decisions can come within 24 to 48 hours for straightforward unsecured applications. High street banks take longer, sometimes several weeks, but may offer better rates for established businesses with clean credit histories.

Once you have the funds, treat repayments as a fixed operational cost. Build them into your monthly cash flow plan from day one. Avoid drawing on working capital finance repeatedly without reviewing whether the underlying cash flow issue has been addressed. Short-term borrowing used to patch a structural problem becomes expensive very quickly.

If you are using the funds to cover a VAT bill, consider spreading the cost across the loan term rather than paying in one lump sum. This keeps your cash buffer intact for other operational needs.

Using an FCA-regulated broker gives you access to multiple lenders through a single application and ensures the advice you receive meets regulatory standards. For retail and hospitality businesses, a merchant cash advance can be a particularly practical option because repayments flex with your revenue rather than being fixed.

Key takeaways

Working capital loans are most effective when matched to a specific cash flow need, structured with a clear repayment plan, and chosen with full awareness of total cost including fees and personal liability.

| Point | Details |

|---|---|

| Match product to need | Choose invoice finance for receivables gaps, revolving credit for recurring shortfalls, and term loans for one-off costs. |

| Know the full cost | Always ask for the total repayable amount, including origination fees and any personal guarantee obligations. |

| Prepare a cash flow forecast | A simple three to six month forecast significantly improves lender confidence and approval chances. |

| Use FCA-regulated brokers | Platforms like Swoop and Rangewell give access to multiple lenders and regulated advice in one place. |

| Avoid structural reliance | Short-term finance should address a temporary gap, not substitute for a sustainable cash flow model. |

Why most SMEs borrow wrong and what to do instead

Here is something most finance guides will not tell you directly: the majority of SME owners I speak with focus almost entirely on whether they can get a loan, rather than whether they should take that particular loan at that particular cost.

The personal guarantee issue is where I see the most damage. A loan described as “unsecured” still frequently carries a personal guarantee clause buried in the agreement. That means if your business hits trouble, your personal savings, your home, and your assets are on the line. I have seen business owners sign these without realising the full implication because they were focused on the monthly payment figure rather than the legal terms.

The other mistake is treating working capital finance as a permanent solution to a cash flow problem that is actually structural. If you are borrowing every quarter to cover the same gap, the loan is not solving the problem. It is masking it, and at a cost that compounds over time.

What actually works is layering finance products to match specific needs, as combining invoice finance with short-term loans allows businesses to cover day-to-day needs flexibly rather than relying on a single large facility. Pair that with a proper cash flow forecast and regular conversations with your broker or lender, and you are managing finance proactively rather than reactively.

Borrow with a clear operational objective. Know what the money is for, when it will be repaid, and what the total cost is. That discipline separates businesses that use finance well from those that get trapped by it.

— Amir

How Switch-and-save helps retail and hospitality SMEs manage cash flow

Managing cash flow is not just about borrowing. It is also about having clear, real-time visibility of your sales, stock, and revenue so you can spot gaps before they become crises.

Switch-and-save provides AI-powered EPOS systems built specifically for UK retail and hospitality businesses. With real-time sales reporting, integrated payment processing, and cloud-based dashboards you can access from anywhere, you get the financial visibility that makes cash flow planning far more accurate. Better data means better borrowing decisions. When you know exactly what your revenue looks like week by week, you can time loan applications, manage repayments, and avoid unnecessary borrowing altogether. Explore the full range of Switch-and-save EPOS packages to find the right fit for your business.

FAQ

What is a working capital loan in the UK?

A working capital loan is a short-term finance product used to cover day-to-day business expenses such as payroll, stock, and utility bills. It is designed to bridge cash flow gaps rather than fund long-term investments.

How much can I borrow with a working capital loan?

UK working capital loans typically range from £5,000 to £500,000, with loan terms from three months to five years. The amount you can borrow depends on your turnover, credit score, and trading history.

How quickly can I get a working capital loan in the UK?

Many alternative lenders and broker platforms offer decisions within 24 to 48 hours for unsecured working capital products. High street banks generally take longer but may offer lower rates.

Do I need collateral for a working capital loan?

Not always. Many working capital loans are unsecured, but lenders may still require a personal guarantee as security. Always check the loan agreement carefully before signing.

What is the difference between invoice finance and a merchant cash advance?

Invoice finance releases a percentage of unpaid invoice value and suits B2B businesses waiting on client payments. A merchant cash advance is repaid as a share of card sales and works best for retail or hospitality businesses with high card transaction volumes. You can compare both options in detail in this invoice finance vs merchant cash advance guide.