A merchant cash advance UK is a form of business funding where a lender advances a lump sum against your future card sales, with repayments automatically deducted as a fixed percentage of daily card transactions until the agreed total is repaid. Unlike a traditional bank loan, there are no fixed monthly instalments and no set repayment date. Funds typically arrive in your account within 24 to 48 hours of approval, making this one of the fastest forms of short-term business funding UK businesses can access. The industry term for this product is a merchant cash advance (MCA), sometimes called a business cash advance UK. It suits retailers, hospitality operators, and service businesses with consistent card turnover who need capital quickly and without the paperwork burden of conventional lending.

How does a merchant cash advance work for UK small businesses?

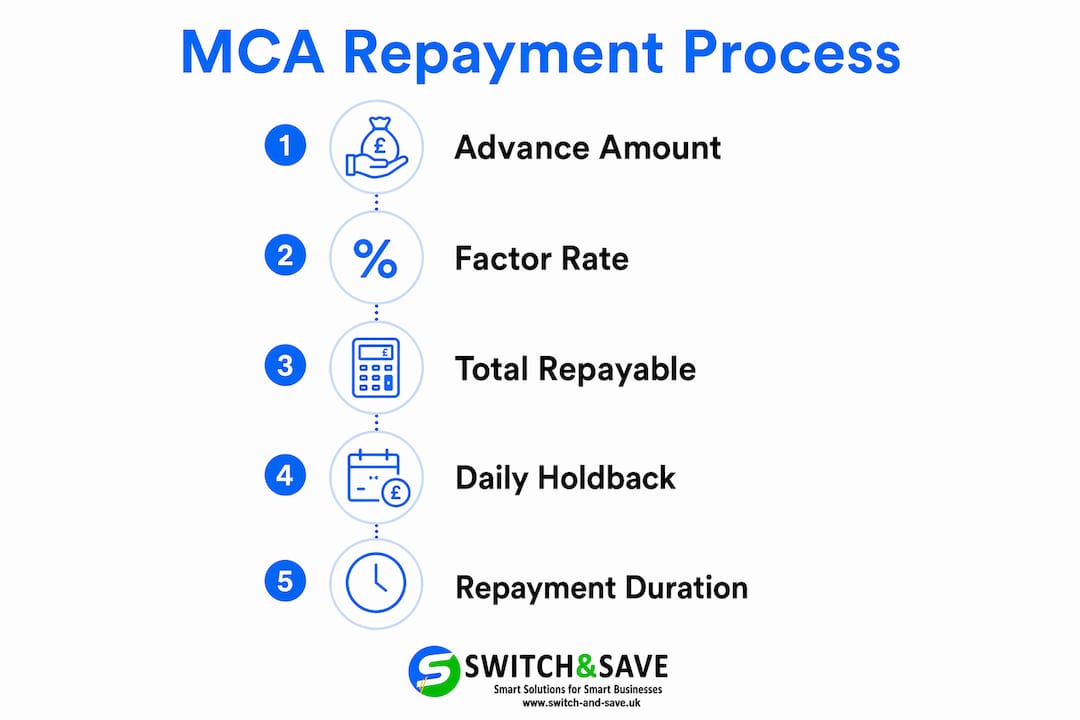

The mechanics of an MCA are straightforward once you understand the three moving parts: the advance, the factor rate, and the holdback percentage.

- You apply based on card turnover. Lenders assess your recent card payment history rather than your credit score or business assets. Most providers ask for three to six months of card processing statements. The stronger your card turnover, the larger the advance you can access.

- You receive a lump sum. Once approved, the agreed amount lands in your business account. Funds typically arrive within 24 to 48 hours, which is considerably faster than a standard bank loan application.

- Repayments are deducted automatically. Your card processor or terminal deducts a fixed percentage of each day’s card takings. This is called the holdback rate, and it typically sits between 10% and 20% of daily card receipts. On a slow Tuesday, you repay less. On a busy Saturday, you repay more.

- The advance is settled when the total repayable is cleared. There is no calendar deadline. Repayment duration depends entirely on your sales volume, which means repayments flex with revenue rather than working against your cash flow.

- Pricing uses a factor rate, not an interest rate. A factor rate of 1.3 on a £20,000 advance means you repay £26,000 in total. The difference between the advance and the total repayable is the cost of the funding.

Pro Tip: Before you sign, ask the lender to confirm the exact holdback percentage and the total repayable amount in writing. These two numbers tell you everything you need to know about the real cost and the likely repayment timeline.

Understanding how merchant cash advances work in practice helps you plan your cash flow and avoid surprises once repayments begin.

What are the typical costs and repayment terms?

Cost transparency is where MCAs can catch business owners off guard. The pricing structure looks simple on the surface but requires careful modelling before you commit.

Factor rates explained

Factor rates typically range from 1.1 to 1.5. A rate of 1.1 means you repay 10% more than you borrowed. A rate of 1.5 means you repay 50% more. The total repayable is fixed at the point of agreement, regardless of how quickly you clear it.

| Advance amount | Factor rate | Total repayable | Cost of funding |

|---|---|---|---|

| £10,000 | 1.1 | £11,000 | £1,000 |

| £10,000 | 1.3 | £13,000 | £3,000 |

| £20,000 | 1.3 | £26,000 | £6,000 |

| £20,000 | 1.5 | £30,000 | £10,000 |

The APR problem

Because MCAs use factor rates rather than annual percentage rates, direct cost comparisons with term loans are not straightforward. The equivalent APR of an MCA depends on how fast you repay. Repay in three months and the effective APR is very high. Repay over twelve months and it looks more reasonable. Term loans may carry effective APRs of around 12% to 18%, while MCAs can carry equivalent APRs from 20% to 80% depending on repayment speed. That is a significant difference, and it matters when you are comparing merchant funding options.

Holdback rates and cash flow

Repayment rates commonly range from 10% to 20% of daily card transactions. A 15% holdback on £2,000 of daily card sales means £300 leaves your account that day. Model this against your operating costs before agreeing to the advance.

Rolling over or topping up

This is the area where costs can escalate quickly. Rolling over an MCA resets the factor rate on the new total, including any outstanding balance. Any repayment progress you made on the original advance is effectively erased. Avoid rolling over unless you have modelled the cumulative cost carefully.

Pro Tip: Use a simple spreadsheet to model three repayment scenarios: fast (four months), medium (eight months), and slow (twelve months). This gives you a realistic range of effective APRs and helps you decide whether the cost is justified for your specific need.

Which businesses qualify for a merchant cash advance in the UK?

Eligibility for a UK cash advance is more accessible than most traditional lending products, but there are still clear thresholds to meet.

- Trading history: Most providers require a minimum of three to six months of UK trading history. Some specialist lenders will consider newer businesses if card turnover is strong.

- Monthly card sales: The minimum threshold varies by lender but typically falls between £1,000 and £10,000 per month in card takings. Higher turnover unlocks larger advances.

- Credit profile: Poor credit and County Court Judgements (CCJs) can be considered by many MCA providers. Eligibility focuses on card turnover and trading history rather than credit scores or asset security.

- Payment processors accepted: All major UK card terminals and processors are generally accepted, including Worldpay, Barclaycard, SumUp, and Square. E-commerce gateways such as Stripe and PayPal are also accepted by most providers.

- Business type: UK-registered limited companies and sole traders in retail, hospitality, and service industries are the most common applicants. Seasonal businesses with variable revenue are particularly well suited because repayments scale with card takings.

- Personal guarantees: Some lenders request a personal guarantee, particularly for larger advances. Always read the terms carefully before signing.

If you are unsure whether your business meets the criteria, the application process guide from Switch-and-save walks through what documentation you will need and how to present your card turnover history effectively.

How does a merchant cash advance compare with other financing options?

Choosing the right funding product depends on your business situation. Here is how MCAs sit alongside the most common alternatives for UK small businesses.

| Feature | Merchant cash advance | Term loan | Invoice finance | Overdraft |

|---|---|---|---|---|

| Repayment structure | % of daily card sales | Fixed monthly payments | % of invoice value | Flexible, interest on balance |

| Speed of funding | 24 to 48 hours | Days to weeks | 24 to 72 hours | Instant (if pre-approved) |

| Credit check required | Minimal | Yes, often strict | Moderate | Yes |

| Security required | No | Often yes | Invoices as security | Sometimes |

| FCA regulated | Generally no | Yes | Yes | Yes |

| Best suited for | Card-heavy businesses needing fast cash | Planned, long-term investment | B2B businesses with unpaid invoices | Short-term working capital |

The regulatory point deserves attention. MCAs are not typically regulated by the Financial Conduct Authority and fall outside standard consumer credit law. The FCA’s Consumer Duty guidance stresses fair value and pricing transparency, but MCA providers are not legally bound by the same disclosure rules as regulated lenders. This means you carry more responsibility as a borrower to scrutinise the terms yourself.

For a detailed side-by-side analysis, the MCA versus traditional loans comparison covers the cost and flexibility trade-offs in depth.

MCAs are most suitable when you need fast access to capital, have strong card turnover, and can absorb a daily holdback without disrupting operations. They are less suitable for long-term investment or businesses with thin margins where a daily deduction would create pressure.

Key takeaways

A merchant cash advance suits UK businesses with strong card turnover that need fast, flexible funding, but the factor rate pricing means true costs must be modelled carefully before committing.

| Point | Details |

|---|---|

| Repayments flex with sales | Holdback rates of 10% to 20% mean you repay less on quiet days and more on busy ones. |

| Factor rates set total cost | A rate of 1.1 to 1.5 determines the fixed total repayable, regardless of repayment speed. |

| Credit score is not the barrier | Eligibility centres on monthly card turnover and trading history, not assets or credit profile. |

| Rolling over increases costs | Topping up or rolling over resets the factor rate on the full balance, erasing prior repayment progress. |

| MCAs are largely unregulated | Unlike term loans, MCAs fall outside FCA regulation, so scrutinise all terms yourself before signing. |

Why I think most small businesses misread the true cost of an MCA

From working closely with UK retail and hospitality businesses, the single most common mistake I see is treating the factor rate as equivalent to an interest rate. It is not. A factor rate of 1.3 sounds modest until you realise that if you repay in four months, the effective APR is closer to 90%. That is not a reason to avoid MCAs entirely. It is a reason to be precise about why you are using one.

The businesses that use MCAs well treat them as a short-term operational tool, not a long-term finance strategy. A café owner covering a kitchen refurbishment before the summer season, or a retailer stocking up ahead of Christmas, can justify the cost because the return on that capital is clear and fast. The businesses that struggle are those who roll over advances repeatedly without modelling the cumulative cost. Small additions to the balance compound quickly when each top-up carries a new factor rate.

My practical advice: model the repayment impact on your daily cash flow before you agree to anything. If a 15% holdback on your average card takings leaves you short on wages or supplier payments, the advance is too large or the holdback rate is too high. Negotiate both. And always ask for the total repayable amount in writing before you sign, along with the exact logic for when the advance is considered fully settled.

If you are genuinely unsure whether an MCA is the right fit, compare it against invoice finance or a government-backed scheme. The Growth Guarantee Scheme offers lower effective rates for eligible businesses and is worth checking before committing to higher-cost merchant funding options.

— Amir

How Switch-and-save can support your business alongside your funding

If you are using a merchant cash advance to invest in your business, the quality of your card payment setup matters more than ever. Your repayments are calculated directly from your card takings, so a reliable, accurate EPOS system is not just convenient. It is central to how your advance is managed.

Switch-and-save offers a range of EPOS systems built for UK retail and hospitality businesses, combining integrated payment processing with real-time sales tracking and cloud-based reporting. Whether you run a shop, a café, or a multi-site operation, the right EPOS setup helps you monitor card turnover accurately, which is exactly the data your MCA provider will use to assess and manage your advance. Explore the full range at Switch-and-save or contact the team for a free demo tailored to your business.

FAQ

What is a merchant cash advance in the UK?

A merchant cash advance is a form of business funding where a lender advances a lump sum repaid through a fixed percentage of your daily card sales. It is not a loan but the purchase of future card receivables, with no fixed repayment schedule.

How quickly can I get funds from a UK cash advance provider?

Funds typically arrive within 24 to 48 hours of approval, making MCAs one of the fastest forms of short-term business funding available to UK small businesses.

Do I need good credit to qualify for a merchant cash advance?

No. Most UK MCA providers focus on your monthly card turnover and trading history rather than your credit score. Poor credit and CCJs can still be considered by many lenders.

What is a factor rate and how does it affect what I repay?

A factor rate is a multiplier applied to your advance to calculate the total repayable. A factor rate of 1.3 on a £10,000 advance means you repay £13,000 in total, regardless of how quickly you clear it.

Is a merchant cash advance regulated by the FCA?

Generally, no. MCAs fall outside standard FCA regulation and consumer credit law, which means you should scrutinise all terms carefully yourself, particularly the total repayable amount and holdback percentage, before agreeing to any advance.