Picking a payment terminal is one of those decisions that looks simple until you get it wrong. Most UK business owners focus on the upfront hardware cost and miss the bigger picture entirely. The right payment terminal UK businesses rely on affects queue times, cash flow timing, customer experience, and how well your systems talk to each other. Get it right and you barely notice it. Get it wrong and it costs you customers, time, and money every single day. This guide covers everything you need to make a confident, informed decision for your retail or hospitality business.

Table of Contents

- Key takeaways

- Types of payment terminal for UK businesses

- Understanding the real costs of payment terminals

- Features that actually make a difference

- Emerging payment options worth knowing

- How to choose and implement a terminal without regret

- My honest take after working with UK retailers and hospitality businesses

- See how Switch-and-save can help your business

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Terminal type must match your setting | Countertop, portable, and mobile terminals each suit different business environments and transaction volumes. |

| True costs go beyond hardware | Processing fees, PCI compliance, and monthly charges can add up significantly beyond the initial purchase price. |

| Features drive operational efficiency | Dual connectivity, next-day settlement, and EPOS integration directly affect checkout speed and cash flow. |

| Emerging alternatives reduce fees | Pay by Bank and hybrid models offer lower fees, immediate settlement, and no chargeback risk. |

| Contract terms matter as much as price | No lock-in contracts with clear settlement terms protect your business from costly surprises. |

Types of payment terminal for UK businesses

Not all card machines are built for the same environment. The three main categories each have a distinct purpose, and choosing the wrong one for your setting is one of the most common and avoidable mistakes.

Countertop terminals are fixed to a till point and connect via broadband or ethernet. They suit high-volume retail settings where customers come to a desk to pay. Think a convenience store, a pharmacy, or a clothing boutique. They are generally the most reliable in terms of connectivity, and they process transactions quickly. The downside is that they are not flexible. If your customer needs to pay at their table or across a large shop floor, a countertop terminal will not work for you.

Portable wireless terminals use Wi-Fi or Bluetooth and allow your team to take payments anywhere within range. These are the natural fit for hospitality settings, from restaurants and cafés to hotel check-in desks. The ability to take payment at the table removes an unnecessary step that slows the end of service. It also feels more professional to the customer.

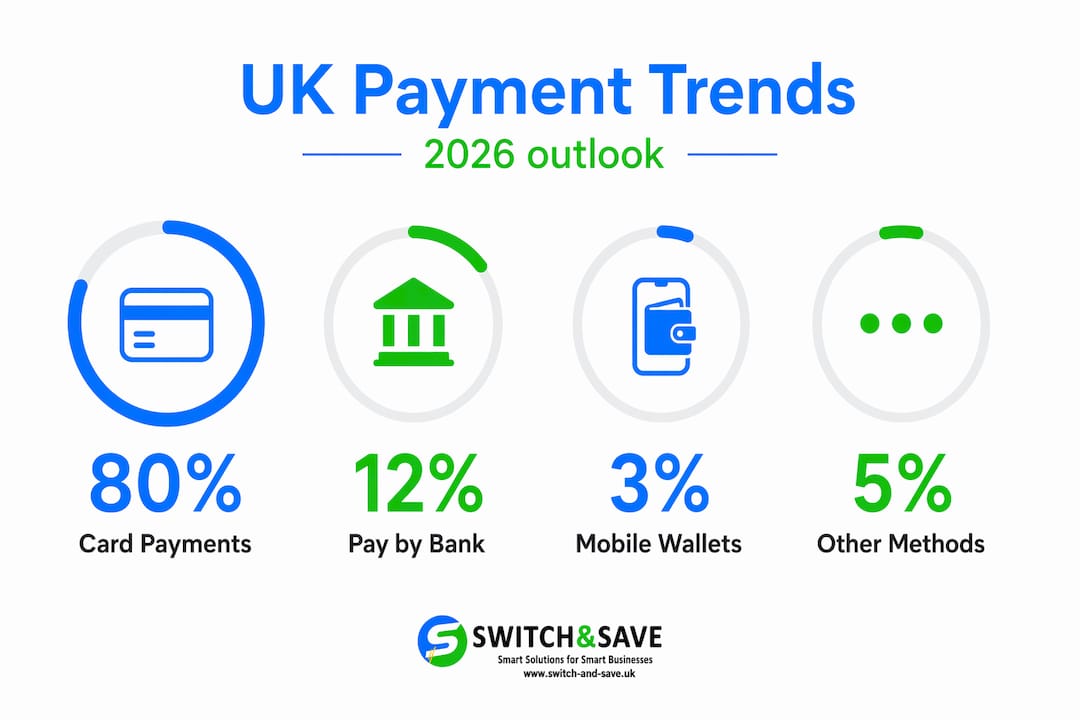

Mobile card readers connect via 4G and are designed for traders who move around. Markets, pop-up stalls, food trucks, catering events, outdoor festivals. If you do not have a fixed location, this is your category. They are compact, often work with a smartphone app, and can process payments almost anywhere there is a signal. Payment processing UK through mobile readers has grown sharply since 2020, and the technology has matured considerably.

When comparing your options, consider these factors:

- Transaction volume. A busy high street retailer processing hundreds of transactions per day needs a different terminal to a market trader doing thirty.

- Connectivity reliability. A Wi-Fi-only terminal in a hospitality venue with patchy coverage creates risk. Dual 4G and Wi-Fi options give you a fallback.

- Customer payment preferences. Contactless, chip and PIN, Apple Pay, Google Pay. Your terminal needs to handle all of them.

- Counter space and mobility. Will staff carry the device to the customer, or will the customer always come to the till?

For a more detailed breakdown of how these types compare across retail and hospitality, the payment terminal guide from Switch-and-save covers the specifics well.

Understanding the real costs of payment terminals

Here is where most business owners get caught out. The upfront cost of hardware is just the beginning.

UK card processing fees typically range from 0.3% to 0.8% for debit card transactions and 0.7% to 1.75% for credit card transactions. On top of that, you will usually pay authorisation fees of 1p to 5p per transaction, a monthly rental or service fee of anywhere between £0 and £40, and PCI compliance costs of up to £20 per month. Chargeback handling fees range from £10 to £25 per dispute.

Those amounts do not sound dramatic individually. But multiply them across your monthly transaction volume and the picture changes quickly.

| Cost type | Typical range | Notes |

|---|---|---|

| Debit card processing | 0.3% to 0.8% per transaction | Lower than credit due to interchange regulation |

| Credit card processing | 0.7% to 1.75% per transaction | Varies by card type and provider |

| Monthly service fee | £0 to £40 | Depends on contract and provider |

| PCI compliance | £0 to £20 per month | Required for all card-accepting businesses |

| Chargeback fee | £10 to £25 per dispute | Charged even if you win the dispute |

| Authorisation fee | 1p to 5p per transaction | Often buried in small print |

One legal point worth knowing: UK regulations ban surcharging card payments, meaning you cannot pass processing fees onto customers. Those costs are yours to absorb. That makes choosing a competitive merchant account UK provider more important than many business owners realise.

Pro Tip: Before signing any merchant services UK agreement, ask for the full schedule of fees in writing, including authorisation fees, chargeback fees, and any monthly minimums. Providers are not always forthcoming with these unless you ask directly.

To get a clearer picture of where costs can be reduced, Switch-and-save’s guide on reducing card machine fees is worth reading before you commit to a provider.

Features that actually make a difference

Once you understand cost, the next question is which features have a real-world impact on how your business runs.

Dual connectivity. A terminal with both 4G and Wi-Fi does not just sound good on a spec sheet. It means your payment processing UK capability does not go down when the broadband drops. For a busy café or restaurant, a terminal going offline during the lunch rush can cost you real money in abandoned sales. Contactless processing speeds can be under two seconds with the right hardware, which matters when you have a queue.

Settlement speed. Next-working-day settlement rather than T+2 or T+3 means your takings are in your account faster. For small businesses managing tight cash flow, this is not a minor detail. It is the difference between paying a supplier on time or not. When reviewing providers, check whether “next day” applies on weekends and bank holidays or only on working days. Many providers exclude weekends from their settlement schedules, which matters if your busiest trading days are Saturday and Sunday.

PCI DSS compliance. All UK businesses accepting card payments must comply with Payment Card Industry Data Security Standards. A terminal that is PCI DSS Level 1 certified reduces your liability and removes the burden of managing compliance yourself. Ignoring this is not worth the risk.

EPOS integration. This is where payment processing UK stops being just about taking money and starts being about running your business better. When your terminal talks directly to your EPOS system, every sale updates stock levels automatically, sales data flows into your reports in real time, and end-of-day reconciliation takes minutes rather than an hour. The benefits of EPOS integration for retail and hospitality are significant, and a terminal that sits in isolation from your other systems is a missed opportunity.

Pro Tip: Ask any card machine provider UK whether their terminal integrates natively with your EPOS software, or whether it requires a third-party payment gateway UK connector. Native integrations are more reliable and faster.

Key features to confirm before you buy:

- Dual 4G and Wi-Fi connectivity

- PCI DSS Level 1 certification

- Contactless including Apple Pay and Google Pay

- Next-working-day settlement with clear weekend policy

- Native EPOS integration or API availability

Emerging payment options worth knowing

The payment landscape is shifting, and card machines are no longer the only option on the table.

The Pay by Bank model is one of the more significant developments for UK merchants. Unlike card payments, which pull funds from a customer’s account and carry chargeback risk, Pay by Bank is a push-based payment. The customer initiates the transfer directly. The result is immediate settlement, no post-payment reversals, and fees that are typically flat or much lower than card processing rates.

“Pay by Bank represents a structural shift in how UK businesses can receive money. It removes the intermediary cost layer that card networks charge and eliminates the chargeback mechanism entirely.”

For hospitality businesses with higher average transaction values, or retail businesses with tight margins, reduced fees and no chargebacks can make a meaningful difference to profitability.

That said, Pay by Bank is not yet ubiquitous. Customers still expect to pay by card. A hybrid approach works well for many businesses: accepting cards through a standard terminal while offering Pay by Bank as an option for customers willing to use it. This keeps you accessible to all customers while gradually shifting some volume to a lower-cost channel.

If you operate in a sector classed as high risk by payment networks (such as adult entertainment, certain travel categories, or high-ticket electronics), standard merchant accounts may not be available or may be terminated without warning. Specialist payment brokers with relationships across multiple banks can secure a stable merchant account UK in these cases, avoiding the risk of your account being frozen at a critical time.

For a broader view of where top payment solutions are heading in the UK, Switch-and-save’s guide to retail and hospitality options goes into further detail.

How to choose and implement a terminal without regret

Making the right choice is a process, not a single decision. Here is a practical sequence to follow.

Assess your transaction volume and peak periods. A terminal that handles your average day fine but struggles on a Saturday afternoon is still the wrong terminal. Know your busiest periods and plan for them.

Audit your connectivity. If you are relying on Wi-Fi in a venue with thick stone walls or a basement bar, test coverage in the actual payment areas. Never assume.

Check compatibility with your existing systems. Your terminal should work with your current EPOS, or the EPOS system you plan to move to. Mismatched systems create manual workarounds that cost you time every day.

Scrutinise the contract. Prioritise no lock-in or short monthly rolling contracts. Upfront cost is a false economy if you are locked into a provider that does not perform. Read the settlement schedule carefully.

Plan your setup and staff training. A terminal that is misconfigured or not understood by your team creates payment errors, slow queues, and frustrated customers. Budget time for a proper setup and at least a brief training session.

Build a chargeback strategy. Proactive chargeback prevention using transaction analytics is no longer optional for businesses with meaningful card volume. Chargebacks cost money even when you win the dispute.

Pro Tip: When comparing card machine providers UK, ask specifically how they handle terminal faults during trading hours. Response time and replacement policy should be written into your agreement.

For first-time buyers, Switch-and-save’s guide on choosing your first card machine is a straightforward starting point.

My honest take after working with UK retailers and hospitality businesses

I’ve spoken with hundreds of UK business owners about their payment setup, and the pattern I see most often is this: they chose a terminal based on the lowest monthly fee, and then spent months dealing with the consequences.

In my experience, the real cost of a poor terminal is not the fee on the statement. It is the customer who walked out because the queue moved too slowly. It is the 45-minute manual reconciliation at the end of every shift. It is the weekend cash flow gap because settlement excludes bank holidays. Those costs are invisible on a comparison sheet but very visible in practice.

What I have found actually works is starting from operations, not price. What does your busiest hour look like? How does your team currently handle end-of-day? Is your stock management connected to what you sell? When you answer those questions first, the right terminal becomes obvious.

The businesses I have seen get the most value from their payment setup are the ones who treated it as part of their EPOS infrastructure, not a standalone purchase. Integration between your terminal and your EPOS is not a nice-to-have. It changes how quickly you can serve customers and how accurately you can manage your business.

One more thing: chargebacks are a growing problem for UK merchants, and most business owners do not have a plan for them until they receive one. The growing chargeback risk across UK retail means you need to think about dispute management as part of your overall payment strategy, not as an afterthought.

— Amir

See how Switch-and-save can help your business

If you are ready to move beyond the basic card machine comparison and want a payment setup that genuinely works for your business, Switch-and-save has solutions built specifically for UK retail and hospitality. From the retail EPOS system to the hospitality EPOS bundle, every option includes integrated payment terminal support, next-working-day settlement, no long-term lock-in contracts, and full UK-based setup and support. You can also explore the full range of EPOS systems to find the right fit for your size and sector. Book a free demo and see the difference an integrated setup makes.

FAQ

What is the average cost of a payment terminal in the UK?

Hardware costs vary widely, from under £50 for a basic mobile reader to several hundred pounds for a countertop unit. Ongoing costs including processing fees, PCI compliance, and monthly charges often matter more than the upfront price.

Can I pass card processing fees on to my customers?

No. UK Payment Services Regulations prohibit surcharging on card payments. All debit and credit card processing costs must be absorbed by the merchant as a business expense.

How do I know which terminal type suits my business?

Countertop terminals suit fixed retail locations, portable wireless terminals work best in hospitality settings where payment at the table is needed, and mobile card readers are ideal for market traders or mobile businesses needing 4G connectivity on the move.

What is Pay by Bank and how is it different from card payments?

Pay by Bank is a push-based payment model where the customer initiates a bank transfer directly. Unlike card payments, it offers immediate settlement and no chargebacks, with fees typically lower than standard card processing rates.

What should I check before signing a merchant services contract?

Always confirm the full fee schedule in writing, including authorisation fees and chargeback costs. Check whether next-day settlement applies on weekends and bank holidays, and prioritise rolling monthly contracts over long-term agreements.