Picture a busy Saturday afternoon in your café or shop. The queue is growing, a customer’s card keeps failing, and your terminal is freezing at the worst possible moment. It is stressful, it costs you sales, and it damages the impression you worked hard to build. Card payments make up 64% of all UK transactions in 2024, which means getting this right is no longer optional. This guide walks you through everything: what equipment you need, how the process actually works, what fees to watch for, and how to avoid the mistakes that catch so many small businesses off guard.

Table of Contents

- Why modern card payments matter for UK businesses

- What you need to accept card payments: essentials and options

- How card payments really work: step-by-step process

- Common pitfalls and expert tips for smooth card payments

- Perspective: what most card payment guides miss (and why adaptability wins)

- Practical next steps: find your perfect card payment solution

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Cards dominate UK payments | Card payments account for the majority of UK retail and hospitality transactions, especially contactless. |

| Get the right setup | Choose a payment terminal, provider, and fee structure that fit your business—integrated EPOS adds value. |

| Understand transaction flow | Knowing how each card transaction works helps you resolve issues and speed up settlements. |

| Watch out for hidden costs | Check all fees, review contracts regularly, and keep up with PCI compliance to avoid surprises. |

| Stay agile | Regularly review your payment setup to adapt to evolving customer preferences and payment methods. |

Why modern card payments matter for UK businesses

Card payments are not just popular. They are the default. Customers walk into your venue expecting to tap and go. If you cannot offer that, many will simply leave.

The numbers back this up clearly. Card payments are forecast to rise from 64% of all UK transactions in 2024 to 67% by 2034. That is a steady, ongoing shift away from cash that shows no sign of reversing. For retail and hospitality businesses, this means the pressure to have fast, reliable card acceptance in place is only going to increase.

Did you know? Contactless accounted for 75% of debit card transactions and 64% of credit card transactions in January 2025, making it the dominant payment mode across the UK.

What is driving this? Several factors are at play:

- Speed. A contactless tap takes seconds. It keeps your queue moving and your customers happy.

- Hygiene. Post-pandemic habits have stuck. Many customers actively prefer not to handle cash.

- Customer expectation. Especially in hospitality, guests now expect seamless payment as standard.

- Digitalisation. Younger customers increasingly use mobile wallets like Apple Pay and Google Pay alongside physical cards.

You can read more about contactless payments trends on our blog, and the wider picture is well covered in the latest industry news. For a broader look at where technology is heading, AI trends in retail offer a useful perspective on where customer expectations are heading next.

The practical takeaway here is simple. Not offering contactless card payments does not just inconvenience customers. It actively costs you revenue. A customer who cannot pay by card is a customer who walks out.

With the importance of card payments established, let’s look at what you need in place to start taking cards efficiently.

What you need to accept card payments: essentials and options

Getting set up to accept card payments involves three core components: the right hardware, the right software, and a reliable service provider. Miss any one of these and you will have gaps in your setup that cost you time and money.

The three essentials

- Payment terminal (hardware). This is the physical device your customers interact with. It needs to support chip and PIN, contactless, and ideally mobile wallet payments. Our payment terminal guide is a great starting point if you are unsure which hardware suits your setup.

- EPOS or payment software. A good software layer means your terminal does not just take payments. It records them, links to your stock, and produces reports you can actually use.

- Merchant account or payment service provider. This is the account that receives funds from card transactions before they reach your business bank account. Some providers bundle this in; others charge separately.

Understanding your fee structure

Typical fee components for UK card acceptance include a per-transaction percentage, monthly terminal rental, payment gateway or software charges, and PCI compliance costs. Here is a quick breakdown:

| Fee type | What it covers | Typical range |

|---|---|---|

| Transaction fee | Percentage of each sale | 0.3% to 1.75% |

| Terminal rental | Monthly hardware lease | £15 to £50/month |

| Payment gateway | Software/cloud processing | £10 to £30/month |

| PCI compliance | Security certification | Up to £5/month |

These costs vary by provider and contract type. Some offer flat-rate blended fees that are easier to budget for, while others use interchange-plus pricing which can be cheaper for high-volume businesses. Explore your card machine options to compare what is available.

Feature checklist before you commit

Before signing any contract, make sure your setup includes:

- ✅ Contactless and chip & PIN support

- ✅ Mobile wallet acceptance (Apple Pay, Google Pay)

- ✅ EPOS integration for stock and sales tracking

- ✅ Reliable connectivity (WiFi, SIM, or both)

- ✅ Clear receipts and refund capability

For a more detailed comparison, our guide on best card machines UK covers the leading options for different venue types. You can also find useful background on online payment insights to understand how payment expectations differ across channels.

Pro Tip: Choose a provider that scales with you. A terminal that works perfectly for one till in a small café may not serve you well when you open a second location or add a busy outdoor trading season.

Now that you understand the must-haves, let’s walk through how card payments actually work when a customer taps or inserts their card.

How card payments really work: step-by-step process

Most business owners know their terminal works, but very few understand what actually happens in those few seconds between tap and approval. Knowing the flow helps you spot problems early and explain them clearly to your provider when issues arise.

Here is the process from start to finish:

- Card read. The terminal reads the customer’s card data via chip, contactless antenna, or magnetic stripe.

- Data encryption. The terminal immediately encrypts the data to protect it in transit. This is part of PCI compliance.

- Authorisation request sent. The terminal sends the encrypted transaction details to your payment processor via a secure gateway.

- Processor contacts the card network. Your processor (for example, Worldpay or Stripe) communicates with the relevant card network such as Visa or Mastercard.

- Issuing bank approves or declines. The customer’s bank checks available funds and fraud signals, then sends back an approval or decline.

- Response returned. The decision travels back through the network to your terminal in seconds.

- Settlement. Approved transactions are batched and settled, with funds transferred to your merchant account, typically within one to three working days.

As explained in detail by payment processing specialists, each transaction involves multiple parties working in sequence: merchant, processor, card network, and issuing bank. Understanding this chain matters because when something goes wrong, you can identify at which point the failure occurred.

“Secure communication at every stage ensures customer data is protected and your business remains compliant.”

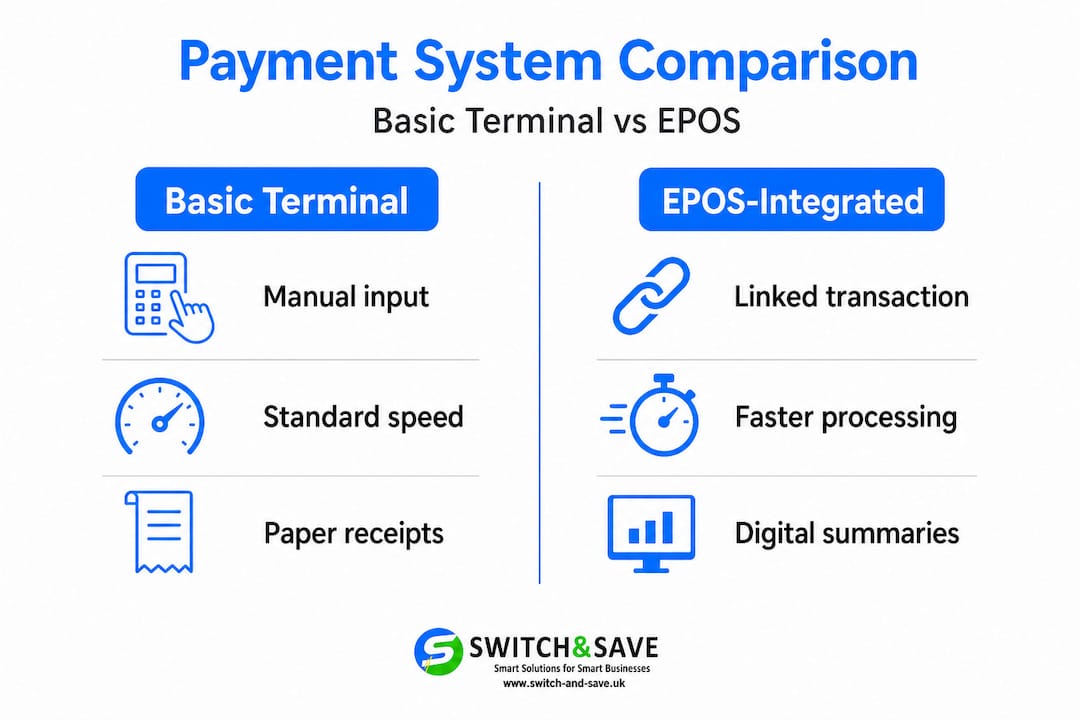

Basic terminal vs EPOS-integrated system: a comparison

| Feature | Basic terminal | EPOS-integrated system |

|---|---|---|

| Transaction speed | Standard | Faster, linked to till |

| Sales reporting | Minimal | Detailed, real-time |

| Stock management | None | Automatic updates |

| Multi-till support | Rarely | Yes |

| Refund processing | Manual | Automated via system |

| Data insights | None | Full cloud dashboard |

If you are still using a standalone terminal, you are leaving a significant amount of operational value on the table. Our guide to choosing your first card machine walks you through the decision in practical terms. For more on how technology is reshaping payment infrastructure, tech solutions for payment processing offers a useful technical backdrop.

With a clear understanding of the payment flow, let’s cover what you can do to keep payments smooth and avoid headaches.

Common pitfalls and expert tips for smooth card payments

Even experienced business owners make avoidable mistakes when it comes to card payments. These errors often seem small at first but add up to real money and real frustration over time.

The most common mistakes

- Ignoring hidden fees. Many contracts include charges that are not obvious upfront. PCI non-compliance fees, minimum monthly service charges, and early termination penalties are common culprits. Always read the full fee schedule before you sign.

- Overlooking PCI compliance. PCI-related charges and compliance requirements are a standard part of card acceptance costs. Failing to meet the standard can result in fines and, far worse, a data breach.

- Choosing the wrong device for your venue. A fixed countertop terminal might suit a small newsagent but would be frustrating in a busy restaurant where tableside payment is expected. Match the hardware to how your business actually operates.

- Neglecting staff training. Your terminal is only as effective as the person using it. Staff who are unsure how to process refunds, deal with declined cards, or troubleshoot connectivity issues will slow down your operation and frustrate customers.

- Not reviewing rates annually. Many businesses accept whatever rate they were quoted on day one and never revisit it. As your transaction volume grows, your provider may be willing to offer better terms. If you do not ask, you will not get.

Expert tips for staying on top of your payments

👉 Always ask for a full fee breakdown before signing, including what happens if you process below a minimum monthly volume.

👉 Bundle where you can. Providers that offer combined hardware, software, and processing fees often give better overall value than piecing together separate services.

👉 Ensure your contract includes clear PCI/DSS compliance support. This is not optional and your provider should help you maintain it.

👉 Prioritise providers with UK-based support. When your terminal goes down on a busy Friday evening, you want to speak to someone who can actually help, quickly.

Understanding exactly what you are paying for is important. Our article on what blended fees mean explains one of the most commonly misunderstood aspects of card payment pricing. And if you are ready to switch providers, our guide to choosing a card machine provider gives you a solid framework to assess your options objectively.

Pro Tip: Set a recurring diary reminder every quarter to review your card payment statement. Look at total fees paid, transaction volumes, and any charges you do not recognise. Over a year, even a 0.3% reduction in transaction fees can add up to hundreds of pounds for a busy small business.

Perspective: what most card payment guides miss (and why adaptability wins)

Most articles on card payments treat the subject like a one-time setup task. Choose a provider, install a terminal, and move on. In our experience working with retail and hospitality businesses across the UK, that mindset is exactly where businesses start losing ground.

Here is the thing: your payment setup is not a utility, like your water supply. It is an active part of your customer experience and your business intelligence. The businesses that understand this perform measurably better over time.

Think about what your EPOS-integrated terminal is actually producing every day. It is recording which products sell fastest at what times. It is tracking staff transaction rates. It is flagging when refunds cluster around a particular product or member of staff. That data has genuine commercial value. But you only access it if you have the right system and you actually look at it.

Forward-thinking retailers we have spoken to revisit their card setup at least once a year. Not just to check they are on a good rate, though that matters too, but to ask bigger questions. Is the checkout experience still as smooth as it could be? Are there payment types customers are requesting that you do not currently support? Is your stock management genuinely integrated with your payment flow, or are there still manual steps that create risk?

Most businesses treat their card machine the way they treat a lightbulb. They ignore it until it breaks, then they react. The businesses that treat it as a strategic asset, something to actively manage and optimise, are the ones that build better customer experiences and stronger margins.

The actionable shift is straightforward. Schedule a quarterly payment review. Bring together whoever handles operations and whoever handles the finances. Look at your data. Ask whether your current setup is still the right fit. Your till should not just be a cash register. It is one of the richest sources of business insight you have.

For a broader look at how payments fit into a wider business strategy, explore our resources in UK payment solutions.

Practical next steps: find your perfect card payment solution

If this guide has prompted you to take a closer look at your current card payment setup, you are already ahead of the curve. Many businesses continue with the same tired terminal and the same unchecked fees for years simply because switching feels complicated. It does not have to be.

At Switch & Save, we specialise in EPOS systems designed specifically for UK retail and hospitality venues. Our solutions combine payment processing, stock management, and real-time reporting in a single integrated package. Whether you run a single-site café or a growing retail chain, our retail EPOS system packages are built to scale with you. For businesses ready to bring payments and operations together seamlessly, our integrated payments bundle offers transparent pricing, UK-based support, and everything you need to move forward with confidence. 👉 Request a free demo today and see the difference a properly integrated system makes.

Frequently asked questions

What are the main fees to watch for in UK card payments?

Expect per-transaction fees, terminal rental, gateway, and PCI compliance costs. These are all standard components of card acceptance in the UK, so always ask for a full fee schedule before committing to a provider.

Why is contactless card payment so important for UK businesses?

Contactless dominates UK card usage, accounting for 75% of debit card transactions and 64% of credit card transactions in January 2025. Businesses that do not offer contactless risk frustrating customers and losing sales to competitors who do.

How long does settlement take for card payments?

Settlement typically takes one to three working days, depending on your provider and account setup. As confirmed by payment processing guides, funds flow to your merchant account after authorisation and batch processing are complete.

What is PCI compliance and do I need it?

PCI compliance is a data security standard that every business processing card payments must meet to protect customer information. PCI-related charges are a standard part of your card acceptance costs, and failing to comply can result in fines or data breaches, so it is not something you can afford to overlook.