If you run a retail shop or hospitality business in the UK, there’s a good chance you’re paying more in card fees than you need to. Most business owners glance at the headline rate on their contract and assume that’s the full story. It isn’t. Interchange fees are regulated for UK consumer cards, but they’re only one slice of what you actually pay. Your provider’s margin, monthly charges, and a string of smaller fees sit on top. This guide will show you exactly where the money goes and how to take back control. Switch&Save card machines offer fully transparent pricing so you always know exactly what you pay.

Table of Contents

- Understanding what drives your card machine costs

- Comparing pricing models: transparent vs flat-rate

- Choosing the right provider and contract to reduce fees

- Practical steps to lower card machine fees today

- Why most UK SMEs overpay on card fees and how to break free

- Save even more on integrated payment solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Breakdown card machine costs | Understanding interchange caps, provider markups, and extra fees is crucial to lowering your total charges. |

| Pricing models matter | Transparent models like Interchange Plus usually offer the best control, but flat-rate may suit smaller businesses. |

| Compare, negotiate, and monitor | Regularly benchmark your contract, negotiate margins, and watch for hidden costs to maintain the lowest rates possible. |

| Actively review providers | Switching or renegotiating providers can quickly reduce your effective fee percentage, especially as your business grows. |

Understanding what drives your card machine costs

Now that you know why many businesses pay more than expected, let’s break down those costs properly.

Every time a customer taps their card at your till, three main parties take a cut. Understanding each one is the first step to reducing your total bill.

The three layers of a card transaction fee:

- Interchange fee: Paid to the cardholder’s bank. For UK consumer debit cards, this is capped at 0.2%, and for consumer credit cards it’s capped at 0.3%. You cannot negotiate this directly.

- Scheme fee: Paid to the card network (Visa or Mastercard). This is small but non-negotiable.

- Acquirer/provider margin: This is what your card machine provider charges on top. This is your main negotiating lever.

The problem is that most providers bundle all three into a single “blended” rate. To understand what blended fees on card machines really mean, and why most merchants get this wrong, read our dedicated guide. You see one percentage, and you assume it’s competitive. But the margin your provider adds can vary enormously, and without a breakdown, you simply cannot tell whether you’re getting a fair deal.

Here’s a typical cost breakdown for a £100 face-to-face debit card transaction:

| Cost component | Approximate rate | Amount on £100 |

|---|---|---|

| Interchange (debit) | 0.20% | £0.20 |

| Scheme fee | ~0.05% | £0.05 |

| Acquirer margin | 0.50% to 1.00% | £0.50 to £1.00 |

| Total effective rate | 0.75% to 1.25% | £0.75 to £1.25 |

As you can see, the interchange cap is just the floor. The real variable is the margin your provider adds. And that’s before you factor in monthly terminal rental fees, minimum monthly service charges, PCI compliance fees, and chargeback handling costs. These are the hidden EPOS system costs that quietly eat into your margins every month.

“The interchange cap is not your effective rate. It’s simply the regulated floor that your provider builds on top of.”

Knowing this distinction is genuinely powerful. It means you’re not powerless. The interchange is fixed, but the margin above it is where the conversation happens. That’s where you can win. If you want to understand how to get how to get low card machine rates, this is the starting point.

Comparing pricing models: transparent vs flat-rate

Knowing what determines your fees, the next step is choosing the right pricing structure.

There are three main pricing models used by UK card machine providers. Each has its place, and choosing the wrong one for your business type can cost you hundreds of pounds a year.

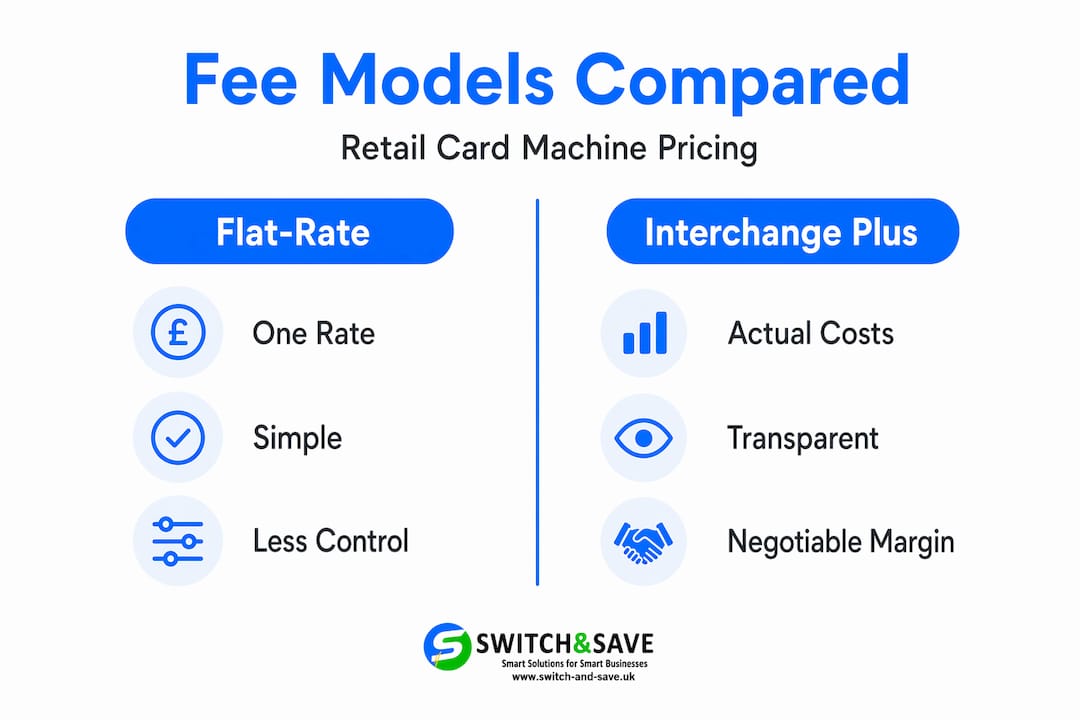

Blended (flat-rate) pricing

One fixed percentage applies to every transaction regardless of card type. Simple to understand, but you lose visibility. You pay the same whether a customer uses a basic debit card or a premium rewards credit card, even though the interchange cost differs significantly.

Tiered pricing

Transactions are grouped into tiers (qualified, mid-qualified, non-qualified) and charged at different rates. Sounds flexible, but providers have wide discretion over which tier a transaction falls into. This model often results in higher costs and less transparency.

Interchange Plus (IC+) pricing

You pay the actual interchange rate plus a fixed provider margin. This is the most transparent model. You can see exactly what the card network charges and what your provider adds on top. Switching to IC+ pricing can help you lower costs because the provider’s markup becomes the only variable you’re negotiating.

Here’s how the models compare for a business processing £10,000 per month in card payments:

| Pricing model | Estimated effective rate | Monthly cost on £10k | Annual cost |

|---|---|---|---|

| Flat-rate (blended) | 1.75% | £175 | £2,100 |

| Tiered | 1.40% to 1.80% | £140 to £180 | £1,680 to £2,160 |

| Interchange Plus | 0.90% to 1.25% | £90 to £125 | £1,080 to £1,500 |

The difference between flat-rate and IC+ can be over £600 a year for a business turning over just £10,000 per month in card payments. For higher-volume businesses, that gap widens considerably. Competitive effective rates for UK face-to-face retail and hospitality commonly land between 0.9% and 1.25% under a well-structured IC+ arrangement.

Which model suits which business?

- Low volume (under £5k/month in card sales): Flat-rate can be simpler and avoids contract complexity.

- Mid to high volume (£5k to £50k+/month): IC+ almost always wins on cost, provided you choose a provider with a competitive margin.

- Mixed card environment (lots of corporate or non-UK cards): IC+ gives you more visibility, which is essential for managing costs.

Pro Tip: Before signing any new contract, ask your provider for a full breakdown of your card mix from the past three months. If a large proportion of your transactions are non-UK or business cards, your effective rate will be higher than the headline figure suggests. Use this data when negotiating. Explore your card payment solutions options before committing.

Choosing the right provider and contract to reduce fees

Once you understand pricing models, the next move is to evaluate your current provider and competitor offers.

Switching providers is not as complicated as many business owners fear. But you do need to compare offers on a like-for-like basis. A lower headline rate from a new provider means nothing if they’re adding a £25 monthly minimum charge or locking you into a 36-month contract with exit fees.

How to vet a provider before switching:

- Request an itemised fee schedule. Ask for interchange, scheme fees, and acquirer margin listed separately. Any provider unwilling to do this is hiding something.

- Check the contract length and exit terms. Short-term or rolling monthly contracts give you flexibility. Long fixed terms can trap you if a better deal appears.

- Identify monthly minimums. Some providers charge a minimum monthly fee regardless of your transaction volume. If you have a quiet month, you still pay.

- Ask about PCI compliance fees. These can add £5 to £30 per month and are sometimes buried in the small print.

- Clarify chargeback and dispute fees. Each chargeback can cost £15 to £25 or more, and some providers charge an admin fee on top.

- Understand the terminal rental cost. Some providers offer “free” terminals but recoup the cost through higher transaction fees.

- Confirm how margin changes are communicated. Some contracts allow providers to increase their margin with 30 days’ notice. This is known as “margin drift” and it’s how many businesses end up overpaying after the first year.

Pay-as-you-go card readers from providers targeting SMEs typically use flat-rate pricing around 1.75%. The fee difference between these providers is often small, but avoiding monthly minimums and long contracts can make a meaningful difference to your annual costs.

Common pitfalls to avoid:

- Signing a multi-year contract without checking the exit clause

- Accepting a verbal rate promise without seeing it in writing

- Ignoring the effect of card mix on your actual effective rate

- Overlooking non-card fees like settlement timing or batch processing charges

Use our switching provider checklist to make sure you cover every angle before you commit. And if you’re still deciding which terminal is right for your setup, our guide to best card machines for UK businesses is a useful starting point. When you’re ready to choose, our guide on choosing a provider walks you through the full process.

Practical steps to lower card machine fees today

With your criteria set, here’s how to take direct action to reduce your fees right now.

You don’t need to overhaul your entire payment setup overnight. These five steps are practical, immediate, and can deliver real savings within weeks.

- Renegotiate your current rate. Call your provider and ask for a better deal. Mention that you’re comparing the market. Many providers will reduce their margin rather than lose you as a customer. This costs nothing and takes 20 minutes.

- Request a full fee audit. Ask your provider for a complete breakdown of every charge over the past 12 months. You may find fees you didn’t know existed. PCI non-compliance charges are a common one.

- Switch to IC+ pricing if you’re on blended rates. If your provider offers IC+ and you’re currently on blended, ask to switch. The savings can be immediate, especially if your card mix is mostly standard UK consumer debit.

- Optimise your card-present transactions. Keyed or card-not-present transactions attract higher interchange rates. If you’re manually entering card details for phone orders, consider moving to a virtual terminal or a proper card-not-present solution that routes correctly.

- Monitor your monthly statements closely. Set a reminder to review your statement each month. Look for new charges, rate changes, or unusual spikes. Small increases add up fast over 12 months.

📊 What a 0.5% fee reduction actually means:

For a business processing £10,000 per month in card payments, cutting your effective rate from 1.75% to 1.25% saves £50 per month. That’s £600 per year. For a business turning over £30,000 per month in card sales, the same reduction saves £1,800 annually. These are real savings that go straight to your bottom line.

It’s worth noting that flat-rate pay-as-you-go readers can be simpler and may win for low-to-mid volumes because they avoid contract complexity and minimum charges. But at higher volumes, or with a favourable card mix, IC+ contracts can outperform significantly. Explore your payment solutions options to find the right fit for your volume and card mix.

Why most UK SMEs overpay on card fees and how to break free

Here’s a candid take on what most UK retailers get wrong, and how to stay ahead.

The uncomfortable truth is that card machine providers rely on inertia. Most business owners sign up, accept the rate, and never look at it again. Providers know this. It’s why margin drift exists. It’s why complex tiered pricing is still common. It’s why monthly minimums are buried in page 14 of a contract.

The headline rate is often a distraction. A provider advertising 0.9% might look cheaper than one advertising 1.2%, but if the first provider charges a £30 monthly minimum, a £10 PCI fee, and a £5 statement fee, the real cost is higher. You have to look at the total annual cost, not just the transaction rate.

Most businesses also never audit their card mix. If you accept a significant volume of corporate cards, non-UK cards, or premium rewards cards, your effective rate will be meaningfully higher than the consumer card interchange cap suggests. Your effective rate depends on your card mix and structure, not just the published rate. This is a critical point that most providers won’t volunteer.

The fix is straightforward, even if it takes some discipline. Benchmark your fees every 12 months. Request a full breakdown from your provider. Compare it against current market rates. If you’re paying above 1.25% effective for predominantly face-to-face UK consumer card transactions, you’re likely overpaying.

Continual benchmarking is the only reliable way to stay competitive. The market changes. New providers enter. Margins shift. A rate that was fair two years ago may be above market today. Our guide to low rates strategies gives you a framework for doing this efficiently without spending hours on it every month.

Save even more on integrated payment solutions

Ready to act? Here’s how integrated solutions can help cut costs even further.

Reducing your card machine fees is a great start, but the biggest gains often come from integrating your payment processing directly with your EPOS system. When your payments and point-of-sale work together, you eliminate manual reconciliation errors, speed up checkout, and get real-time visibility over your sales and costs in one place.

At Switch and Save, our EPOS payment systems are built specifically for UK retail and hospitality businesses. We combine AI-powered software, integrated payment processing, and transparent pricing into one streamlined package. Our integrated payment bundles are designed to help SMEs lock in lower processing costs while simplifying day-to-day operations. Book a free demo today and see exactly how much you could save.

Frequently asked questions

Are card machine fees negotiable for UK businesses?

Yes, fees above the interchange cap are often negotiable. Your negotiable lever is typically your provider’s acquirer margin and any monthly or per-transaction extras they charge on top.

What are the typical card machine fees for small UK shops?

SMEs with transparent pricing commonly see effective card fees in the 0.9% to 1.25% range for face-to-face consumer debit and credit. Competitive effective rates land in this range when structured properly under Interchange Plus pricing.

Is flat-rate pricing better than interchange-plus for small volumes?

Flat-rate pay-as-you-go readers can be simpler and often win for lower volumes since they avoid minimums and complex contracts, though interchange-plus can be cheaper at scale.

What hidden costs should I check before switching card machine providers?

Always look for setup charges, monthly minimums, non-cancellable contract terms, PCI compliance fees, chargeback handling charges, and transaction surcharges that can inflate your effective rate well above the headline figure.

Do interchange caps apply to all card payments in the UK?

No. UK consumer debit interchange is capped at 0.2% and consumer credit at 0.3%, but these caps do not apply to business cards, corporate cards, or non-UK issued cards, which can carry significantly higher interchange rates.