Eligible UK businesses may be able to access £5,000 to £1,000,000 with a merchant cash advance through YouLend, depending on business revenue, card sales, trading history, affordability checks, and provider approval.

A merchant cash advance is usually repaid through a fixed percentage of future sales. This means repayments can move with your business performance. When sales are higher, you repay more. When sales are lower, repayments reduce in line with your takings.

For many UK small businesses, this can be a useful alternative to a traditional bank loan, especially if the business takes regular card payments through a card machine, online checkout, EPOS system, or payment provider.

The easiest way to find out how much your business could be eligible for is to complete a funding eligibility check.

Funding is subject to eligibility, affordability, business performance, provider checks, and approval.

What Is a Merchant Cash Advance?

A merchant cash advance is a flexible type of business funding based on your future sales. Instead of repaying a fixed amount every month like a traditional loan, your repayments are usually taken as a percentage of your daily or regular sales.

This can make it suitable for businesses where revenue changes from week to week or season to season.

For example, a café may have stronger sales during weekends. A takeaway may be busier in the evening. A retail shop may earn more during Christmas, summer, or local events. With a merchant cash advance, repayments are linked to sales activity rather than fixed monthly instalments.

How Much Can You Borrow?

Through Switch & Save’s finance partner YouLend, eligible businesses may be able to access funding from:

£5,000 to £1,000,000

The exact amount depends on your business profile. There is no one fixed answer for every business because each application is assessed individually.

A provider may look at:

| Factor | Why It Matters |

| Monthly revenue | Shows how much money the business generates |

| Card sales | Helps estimate repayment capacity |

| Trading history | Shows business stability |

| Sales consistency | Helps assess risk and affordability |

| Business sector | Some sectors have stronger card payment patterns |

| Existing finance | Existing commitments may affect eligibility |

| Affordability | The advance should not put pressure on cash flow |

The stronger and more consistent your revenue is, the better your chances may be of qualifying for a higher funding amount.

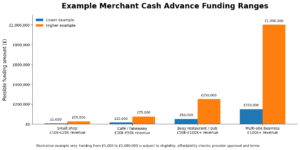

Example Borrowing Scenarios

These examples are only for guidance. They are not guaranteed offers.

| Business Type | Monthly Revenue Example | Possible Funding Direction |

| Small convenience store | £10,000 to £20,000 | May qualify for a smaller advance |

| Café or takeaway | £20,000 to £50,000 | May qualify for medium-level funding |

| Busy restaurant or pub | £50,000 to £100,000+ | May qualify for larger funding |

| Multi-site retail or hospitality business | £100,000+ | May be considered for higher funding |

The only way to know the actual amount your business may be eligible for is to complete an eligibility check.

Check funding eligibility here: Eligibility check

How Do Merchant Cash Advance Repayments Work?

Merchant cash advance repayments are usually linked to your sales.

For example, if your business agrees to repay 10% of future sales, then the repayment amount changes depending on how much you sell.

| Daily Sales | Repayment Percentage | Amount Repaid |

| £500 | 10% | £50 |

| £1,000 | 10% | £100 |

| £2,000 | 10% | £200 |

This type of repayment structure can be useful for businesses with changing sales patterns. You are not normally locked into the same fixed monthly repayment regardless of trading performance.

Why Your Card Sales Matter

Your card sales are one of the most important factors in a merchant cash advance application.

If your business takes regular payments by debit card, credit card, contactless, or online payment, the provider can use that activity to understand how much your business may be able to repay.

Businesses that may benefit include:

- Retail shops

- Grocery stores

- Mobile phone shops

- Cafés

- Restaurants

- Takeaways

- Pubs and bars

- Salons

- Barbers

- Beauty clinics

- Hospitality businesses

- Online sellers

If your business has very low card sales, you may still be able to apply, but the amount available may be lower. If your business has strong and consistent card sales, your eligibility may improve.

Why Revenue Also Matters

Card sales are important, but overall revenue matters too. Some businesses take payments through multiple channels, such as:

- Card machine payments

- EPOS payments

- Online orders

- Delivery platform payments

- Website sales

- Bank transfers

- Marketplace payments

A provider may consider your wider business performance, not only one payment channel. The more clearly your business can show its revenue, the easier it may be to assess eligibility.

This is where having a reliable EPOS and reporting system can help. A good EPOS setup gives you better visibility over sales, stock, payments, staff activity, and business performance.

Switch & Save provides EPOS systems, card payment solutions, and business utility switching services for UK small businesses.

Merchant Cash Advance vs Traditional Business Loan

A merchant cash advance is different from a traditional business loan.

| Feature | Merchant Cash Advance | Traditional Business Loan |

| Repayment style | Percentage of future sales | Fixed monthly repayments |

| Sales flexibility | Repayments move with sales | Repayments usually stay the same |

| Best for | Businesses with regular card sales | Businesses with predictable cash flow |

| Funding use | Stock, cash flow, equipment, growth | Larger planned investments |

| Cost structure | Fixed fee model | Interest and possible fees |

| Application focus | Sales and revenue performance | Credit profile, accounts, security |

A traditional loan may suit some businesses. However, a merchant cash advance can be helpful for businesses that want repayments linked to their trading activity.

For example, a restaurant may not want a fixed repayment during a quiet month. A retail shop may prefer repayments that rise during busy periods and reduce during slower periods.

What Can You Use the Funding For?

A merchant cash advance can be used for many business purposes, depending on the provider’s terms.

Common uses include:

| Business Need | Example |

| Buying stock | Preparing for a busy season |

| Equipment | Replacing fridges, ovens, tills, or EPOS hardware |

| Refurbishment | Improving a shop, café, restaurant, or salon |

| Marketing | Running local ads or seasonal campaigns |

| Cash flow | Covering short-term business costs |

| Expansion | Opening another location or adding services |

| Supplier payments | Paying suppliers before revenue comes in |

| Hiring | Supporting payroll during growth |

The best use of funding is one that helps your business grow, save money, improve operations, or handle a short-term cash flow gap.

You should avoid borrowing without a clear plan.

How to Estimate What You Might Be Eligible For

Before applying, it helps to review your numbers.

Ask yourself:

- How much revenue does my business make each month?

- How much of that comes through card payments or online payments?

- Are my sales stable, growing, or declining?

- Do I already have business finance repayments?

- How much can I comfortably repay through future sales?

- What will I use the funding for?

- Will the funding help the business generate value?

The amount you can borrow is not only about how much the provider may offer. It is also about how much your business can sensibly manage.

A larger advance may look attractive, but it should not damage your daily cash flow.

Is a Merchant Cash Advance Good for Small Businesses?

A merchant cash advance can be useful for small businesses that:

- Take regular card payments

- Need quick access to working capital

- Prefer flexible repayments

- Have seasonal or variable sales

- Want to avoid fixed monthly repayments

- Need funding for stock, equipment, or cash flow

However, it may not be right for every business.

You should always check:

- Total repayment amount

- Fixed fee

- Repayment percentage

- Estimated repayment period

- Impact on cash flow

- Any provider terms and conditions

Funding should support your business, not create pressure.

How Quickly Can Funding Be Available?

Speed depends on the provider and application details.

YouLend says businesses could have funding approved in as little as 24 hours and access funds in as little as 48 hours after approval.

This can make merchant cash advance funding useful when a business needs to act quickly, such as buying stock, replacing equipment, or dealing with an unexpected business cost.

However, approval and timing are not guaranteed. They depend on the application, checks, and provider decision.

How to Improve Your Chances Before Applying

Before checking eligibility, make sure your business information is clear and up to date.

You may want to prepare:

- Recent sales information

- Card payment history

- Business bank details

- Trading history

- Business registration details

- Owner or director information

- Funding purpose

- Existing finance details

You should also review your EPOS and payment reports. If your sales data is accurate, it becomes easier to understand your business performance.

A modern EPOS system can help you monitor:

- Daily sales

- Card payments

- Cash payments

- Product performance

- Staff activity

- Stock movement

- Reports and trends

This is useful not only for funding, but also for running the business more efficiently.

Where Switch & Save Fits In

Switch & Save supports UK small businesses with EPOS systems, card payment solutions, business finance support, and utility switching services.

For businesses considering a merchant cash advance, Switch & Save can help by connecting eligible businesses to its finance partner YouLend.

This can be useful if your business already takes card payments and wants to explore funding without going through a traditional bank loan route.

Related guides:

How to Get Business Finance in the UK Without a Bank Loan

Business Finance for Startups in the UK: What to Know Before Applying

How Small Businesses in the UK Can Get Funding Using Card Sales

Key Takeaways

| Question | Answer |

| How much can I borrow? | Eligible businesses may access £5,000 to £1,000,000 through YouLend. |

| Is approval guaranteed? | No. Funding is subject to eligibility and provider approval. |

| What affects the amount? | Revenue, card sales, trading history, affordability, and business performance. |

| How are repayments made? | Usually through a fixed percentage of future sales. |

| Is it a traditional bank loan? | No. It is a flexible funding option linked to sales. |

| How do I check my amount? | Complete an eligibility check through the YouLend application link. |

Check Your Funding Eligibility

The fastest way to find out how much your business could be eligible for is to complete an online eligibility check.

Eligible UK businesses may be able to access funding from £5,000 to £1,000,000 through YouLend.

Check funding eligibility here: Apply through Switch & Save’s YouLend partner link

Funding is subject to eligibility, affordability checks, business performance, provider approval, and terms and conditions.

FAQs

How much can I borrow with a merchant cash advance?

Eligible businesses may be able to access funding from £5,000 to £1,000,000 through YouLend. The actual amount depends on revenue, card sales, trading history, affordability, and approval.

What affects how much I can borrow?

The main factors are your monthly revenue, card sales, sales consistency, trading history, existing finance, business sector, and repayment affordability.

Do I need card sales to qualify?

Card sales are usually important because merchant cash advance repayments are often linked to future sales. Businesses with regular card payments may be better suited to this type of funding.

Are repayments fixed every month?

Usually no. Repayments are commonly taken as a fixed percentage of future sales, so they can rise and fall with your business takings.

Can I get funding if my business is seasonal?

Possibly. Seasonal businesses may still be considered, but the provider may review trading patterns carefully to understand average revenue and affordability.

Is a merchant cash advance the same as a business loan?

No. A merchant cash advance is different from a traditional business loan because repayments are usually linked to future sales rather than fixed monthly instalments.

How quickly can I receive funding?

YouLend says approval may happen in as little as 24 hours and funds may be available in as little as 48 hours after approval. This depends on provider checks and application status. (YouLend)

Can I use the funding for stock or equipment?

Yes, many businesses use merchant cash advance funding for stock, equipment, refurbishment, marketing, cash flow, supplier payments, or business growth.

Is approval guaranteed?

No. Funding is subject to eligibility, affordability checks, provider approval, and terms and conditions.

How do I check if I am eligible?

You can check eligibility online through Switch & Save’s YouLend partner link:

Check funding eligibility

So, how much can you borrow with a merchant cash advance?

Through Switch & Save’s finance partner YouLend, eligible UK businesses may be able to access £5,000 to £1,000,000. The final amount depends on your revenue, card sales, trading history, affordability, and provider approval.

A merchant cash advance can be a practical option for businesses that take regular card payments and want flexible repayments linked to future sales. It may help with stock, equipment, refurbishment, cash flow, marketing, or growth plans.

The best next step is simple: check your eligibility and see what your business could qualify for.

Switch & Save helps UK businesses reduce costs with EPOS systems, card payment solutions, business finance support, and utility switching services. Check your savings today.